An angry buying agent has used social media to warn purchasers to “never, ever, ever deal with a mortgage broker who works in or with an estate agent”.

Henry Pryor, who has over 25,000 followers on Twitter, also tweeted: “Mainstream estate agent tells me that if I make an offer my client will need to speak to their mortgage advisor to confirm they have funds.”

On Twitter Pryor identified the firm as Spicerhaart, describing it as “incompetent” and “naughty”. However, last night Spicerhaart said that all procedures had been followed correctly.

Pryor told EYE that his client already had a mortgage agreed in principle (AiP) when he made an offer on their behalf for a property being sold by haart.

The offer was confirmed in writing, together with details of the client, their lawyers, mortgage broker, a copy of the AiP, and details of timing.

Pryor says he was then told the offer could only be put forward after the buyer was ‘qualified’ by a mortgage broker. Details were sent – unasked, says Pryor – to a broker at Just Mortgages, a subsidiary of Spicerhaart.

Pryor complained but forwarded a copy of the AiP to the broker and agent.

The agent then emailed Pryor’s client to ask for their date of birth and copies of bank statements.

Pryor called the haart branch concerned and was told the information was required to make Anti-Money Laundering checks on the buyer.

Pryor was then told by email that haart had not been able to qualify the buyer and that the (by then increased) offer had been rejected.

Pryor told EYE that he had a number of questions including:

- Was there a delay in passing over the offer to the vendor pending qualification by the agent’s own broker?

- Was the seller incorrectly told that the buyer had not been ‘qualified’?

- Was advice given to the seller abut the offer “tainted” by the lack of a mortgage lead?

- Should consent to pass buyers’ details to another company, including subsidiaries, be sought first?

- Why is the buyer’s date of birth required when making an offer?

- Is confirmation from a buyer’s mortgage broker, buying agent or lawyer not good enough for a sales agent to be able to rely on?

- Does a buyer need to be AML checked when making an offer, or once the offer is accepted? When is the start of the business relationship?

- Should an agent really be earning fees from mortgage and conveyancing leads about buyers? Is there a conflict of interest, given that the agent acts for the seller?

Pryor told EYE: “I’m a generous-minded chap, but can we really assume that the Chinese walls between a mortgage broker and a selling agent are soundproof?

“Can a buyer really negotiate if he has had to disclose his financial situation to the other party? Surely it can be done once a deal is agreed?”

We put all these points to Spicerhaart and last night chief executive Paul Smith told EYE: “We cannot comment on the specific details of this case due to client confidentiality but can confirm that all procedures were followed correctly.

“We comply with Anti Money Laundering regulations and our processes are tried and tested with thousands of transactions every year.

“This includes running an identity check on a purchaser, for which we require their date of birth. This takes place once their offer has been accepted and technically forms the start of the business relationship.

“In order to progress any house sale, it is vital that we check that all prospective purchasers have the means to buy the property in question. Many transactions fail at the last hurdle because other agents do not go through this process.

“Our procedures ensure that any potential buyers are qualified before an offer is put forward and this is undertaken within a minimum time frame. If the offer cannot be qualified within that time frame, the offer is put to the vendor with the caveat it still needs to be substantiated.

“We do accept confirmation of an Agreement in Principle from a mortgage broker as a good enough basis for a positive offer substantiation. If this detail were to be supplied by a buying agent or lawyer it would also be acceptable. We also in some instances double check.

“We always obtain consent to pass buyers’ details to another company, or subsidiary, within our group and this is recognised specifically in our offer documentation where approval is sought and granted verbally at registration. Buyers are in no way obligated to use our financial services but can choose to do so.

“Under no circumstances would we say that an offer can only be accepted if we have substantiated it or that the buyer has to arrange their mortgage with us.

“We have an effective complaints procedure if any client believes we have not followed our procedures correctly.”

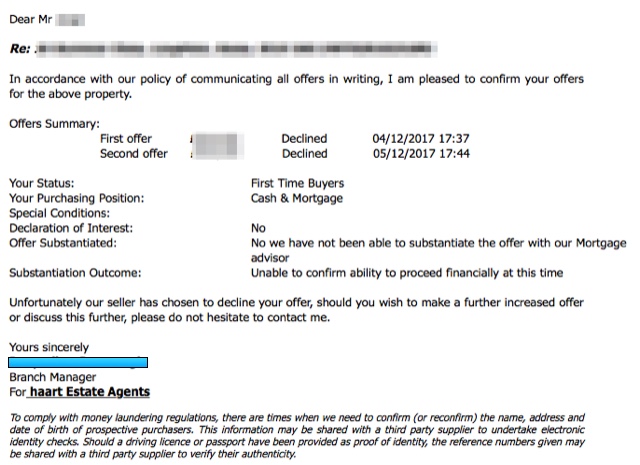

The letter from haart turning down both offers from Pryor’s client is below.

I cannot keep count of the number of times in the past 12 months we have had clients that have claimed to not need qualifying because they have an AIP, only to find out at the point of our broker speaking to them that a) their broker had not mentioned the higher SDLT due to other homes in the background or b) the amount they have claimed to earn to their broker does not marry up with their self assessment income. Any fool can get an AIP, always worth carrying out your own due dil.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Yes, agents should be able to verify that a purchaser is financially able to proceed. But we all know that the checking process is so keenly followed because it provides an opportunity to sell financial services. And even if the buyer has a decent AIP an FA will almost certainly say they can get them a better deal.

Dress it up in whatever way you like, the ‘checking’ process is a smokescreen and the selling of financial services has no place in good agency practice where the first duty is to the client – who should be the sole source of the commission income.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You say the first duty is to the client.

The client is the seller NOT the buyer. Reasonable steps to ensure the buyer can indeed purchase a property is a duty of care for the agents client.

It is very easy to jump online and get an AIP entering in details that are not checked.

I am sure some agents do abuse the service and strong arm buyers to use their mortgage broker but that is not what Henry is complaining about.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

The agent is 100% correct. It is their job to ensure the buyer is suitable for the property and as such should be financially qualified.

They are under no obligation to use the agents broker but must demonstrate they have the means to purchase.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

This has been “a dripping roast” especially for most of the large agency groups for years. So well said Henry!!

Now wait for the push back.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Offer the full asking price and see what happens.

Without details of the property or offers it is difficult to be properly objective about this

I’m not sure I’d be too worried about a buyer’s agent attempting to blackmail me with their twitter presence or media connections

If I were the agent I’d take this as a determined desire to buy the property and would hold out for an acceptable offer safe in the knowledge the applicant has enough money over and above the asking price to employ and pay their own donkey dealer.

If the applicant doesn’t have the means to buy there are lots of more affordable properties available.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

A copy of the AIP and a brief conversation with the buyers mortgage broker/consultant the verify their situation is quite sufficient. If there’s an AIP then there is no more that the agent’s consultant can do that the buyers consultant hasn’t. If he is a qualified mortgage consultant then his verification should be enough. All you need to do is explain to your seller how you have qualified the buyer. In this situation there is absolutely no need for a buyer to have to visit the agents consultant other than to try and close them to use their services. ID for AML is a different matter and yes the agent will need to deal with that.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It seems Mr May has beaten me to the punchline.

Mr Pryor’s Tweets have previously been full of boasts of “saving” his clients mahoosive percentages of a property’s Asking Price (less of course his, I am sure, modest Fee for doing so…).

This won’t be the first time that he has come up against the reality that negotiation often starts with “No!”. Or – in this instance, more’s like “You’re having a laugh, ain’t you?”

What’s not clear here is whether negotiations are still in progress. I suspect not – as if they were, then Mr Pryor’s actions to take this confidential matter to the public domain may well have scuppered his clients’ chances of having an offer accepted in any event.

So that would imply a ‘alternative fact’ – that he low-balled… lost out and now wants to hang the blame on the rest of the industrialised world to his client for his not being able to pull together a deal for them.

And he can wrap his argument in as many layers of Christmas paper as he wants – it can’t disguise the fact that the content of the parcel is brown and nitrogenous…

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I always get either personal evidence – photo driving licence or passport and utility bill( not mobile phone) of clients when they appoint me and also evidence of funds so that I have all the information ready for when we start the negotiations. Or certified copies

One major international London based firms even carries out MLR checks on me when I offer on behalf of retained clients

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Mr Turner

Surely it is a requirement for you to carry out those checks for your own business?

Would you accept those of a third party?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’m sure these “finding agents” also have their own brokers they recommend no? I think it’s clear from the letter the lack in offer is the real issue not the fact they didn’t use their mortgage broker to verify finances. I’m pretty sure spicer haart have sold thousands of homes with out getting a mortgage lead out of it.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Standard practice, I understand, for SH employees to drag applicants in front of their mortgage consultants, whether they need one of not!

I recall a conversation many years ago between a SH neg (who knew the buyer and their circumstances well) and an area manager

SH: Why didn’t they see the mortgage adviser?

Neg: They’re buying cash

SH: We might be able to persuade them to have a mortgage

Neg: They’re wanting to buy cash

SH: They should still have seen ***

Neg: Which part of cash don’t you understand?

Result – bollocking!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You mention this took place many years ago so it may not apply – but – many cash buyers do not realise that they could get a much better return if they were to get a mortgage-or-two whilst rates are at a historical low. They might be better off investing in two BTLs (each with a small mortgage), or a residential and BTL instead of just the one property outright.

Might be something the buyer had not thought of and would have been grateful to have been advised of. *shrug*

Back on topic: There’s certainly pressure on negs to get FS leads over. I’ve worked for corporates that impose FS targets and then pay commission on the leads. It can be very frustrating for buyers (and for negs who want to tie up a deal) when the sales managers twist arms to get bums on seats.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

PeeBee thank you. Only when they are certified by a known legal/accountancy firm when dealing with overseas buyers before I actually meet them in UK.

It is interesting that buyers are beginning to realise they will be checked by more than one company within the buying process.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Poor Henry – he’s lost out on earning his introducer fee and wants to moan about it. Why add an additional layer of expense to a buyer by having a buying agent?? He’s probably on a kickback from his “own” mortgage guy so doesn’t want to lose that.

If the buyer’s own mortgage broker has done a good job then there is no issue with them speaking to another one, we all know it helps the offer to be accepted if we can confidently say they have been qualified by OUR own advisor.

If the qualifying broker/advisor picks up the deal and offers a better service and/or better advice for the buyer so be it – everyone is happy! (Except the cr@p mortgage broker who lost his client and the poncey buying agent who lost his kickback from the said cr@p broker!)

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Interesting article…for me personally, having worked for a number of small independent estate agents and two larger high street models, I am definitely in agreement with those that believe that an AIP from a reputable FA is more than satisfactory for a client, ie; the vendor. In all the years I have been in this business, not once has an AIP for a buyer who is using a mortgage broker outside the firm, never stacked up but when I worked for one of the larger high street agents where I was heavily targeted for FA referrals, this happened on a number of occasions (probably just coincidence but worth mentioning!!). I totally agree with Revilo as this happened to me with the agent in question on this thread and was given a right old rollocking. With the larger high street agents I worked for, you were definitely incentivised and targeted to get a buyer and even somebody that was registering who already has an AIP to see the in house FA and were reprimanded if you did not insist on this happening!!). These firms get so many kickbacks and that is their incentive, IMO!!!!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It should be acknowledged that whilst many are referring (pun intended) to the Corporate model of our industry as being the major culprits for FS targets, pretty much every Agent has an arrangement with an FA that puts some form of meat on the Agent’s table for passing successful business over.

From personal experience and many years of observation I can quite honestly say that a fair few ‘independent’ Agencies are run in a far more corporatesque way than ever the likes of BHA, Nationwide, General Accident or Prudential set out their Numbers Game target bars.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Poke in the Eye for Henry Pryor, poor chap lost out on his commission. No wonder he is pissed off.

Haart followed procedures and are correct in what they done.

If an offer is being put forward the question that needs to be asked of any mortgage broker is how was the AIP carried out.

1. Have bank statements been seen

2. Have payslips been seen

3. Has proof of deposit been seen

Or was it a quick AIP you can do on a lenders website on information provided verbally.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Strange that so many agents don’t understand the estate agents act and what an aip actually is.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I have a hoover called Henry.

He makes a lot of noise and sucks and blows about a bit. Just turn him off when we’ve had enough of him though.

Don’t seem to be able to turn this Henry off !!!!!!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register