The online estate agency industry is not near collapse and Purplebricks’ UK operations are “meaningfully profitable”, a commentator has said.

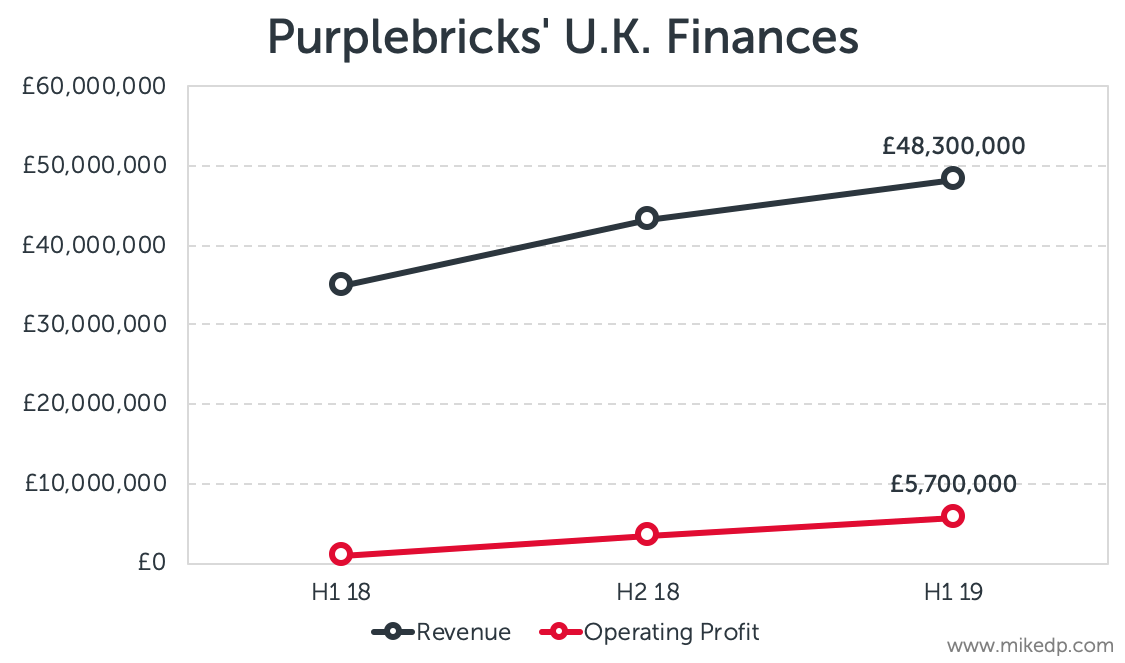

Analyst Mike DelPrete said that last week’s Purplebricks results showed an overall group loss of £27.3m for the first half of its 2019 financial year, with a slight reduction in full-year revenue guidance.

But, says DelPrete: “The top line numbers don’t come close to telling the full story (hint: it’s not as bad as it sounds).

“Purplebricks’ core UK market continues to grow and is meaningfully profitable, proving that the model works.

“Key performance indicators in its other three markets reveal a deeper story of investment growth, and challenges.”

He says that the popular narrative – that the entire online business model is near collapse – “is seductive but factually incorrect”.

He goes on: “Purplebricks is an international collection of businesses at various stages of growth. In the UK, Purplebricks’ most mature market, it continues to grow revenues and operating profit. At maturity and scale the business model absolutely works; there is no evidence to support otherwise.”

DelPrete does say that its rate of growth is slowing in the UK: “But at nearly 80,000 instructions per year, it can’t be expected to keep growing at historic rates. The key is that even in a challenging economic climate, growth continues.”

Purplebricks has had a “bumpy ride” in Australia, he says. There, it must execute a turn-around plan with a new team and pricing activity, after an $18m loss.

In the US, Purplebricks continues to invest heavily, spending over $20m in marketing and sales. It will also need to go from 200 to 650 instructions per month to break even, and to 1,000 to reach profitability.

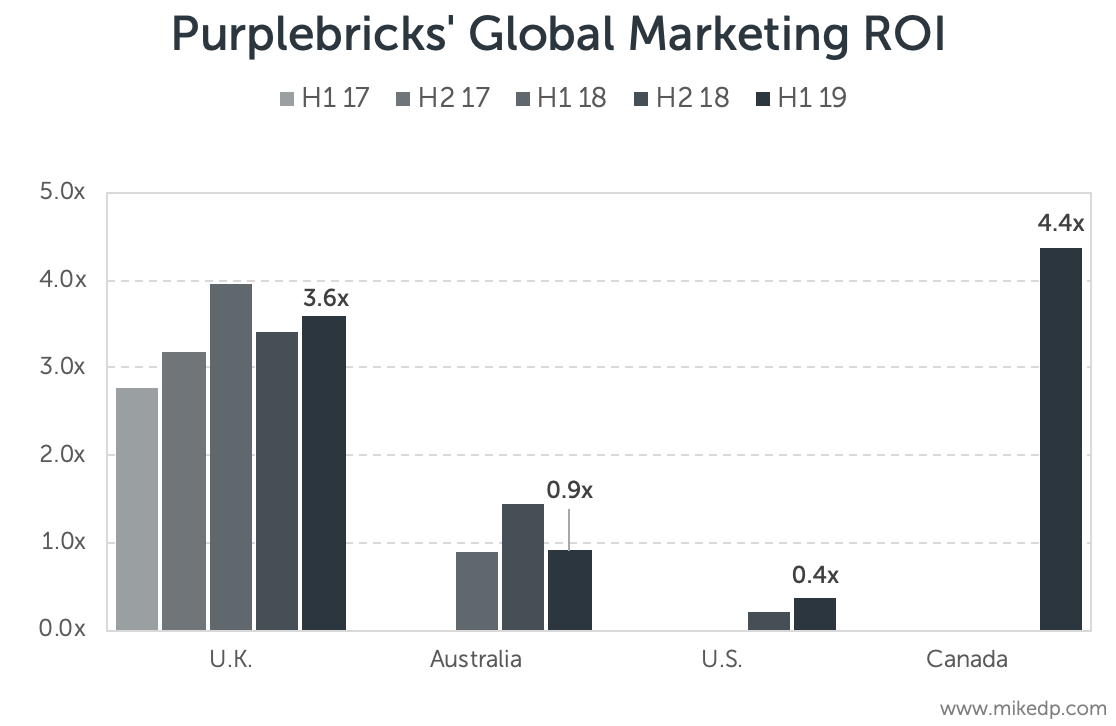

Overall, says DelPrete, Purplebricks “is as much an advertising company as it is a real estate company”.

For every £1 spent on marketing, Purplebricks generates revenues of £3.60 in the UK, £0.92 in Australia, 0.36p in the US, and £4.38 in Canada.

He concludes: “The core Purplebricks business model – and profitability at scale – is sound. The market failure of smaller players, of the fact that Purplebricks is deeply investing in new markets doesn’t diminish that fact.”

DelPrete says that Purplebricks is willing to invest tens of millions year after year to build market share, incurring big losses along the way.

He queries: “If you’re a traditional real estate agency, or a listed company, are you willing to do the same?”

Meanwhile, another analysis questions whether Purplebricks shares should be snapped up at their current price.

On the Motley Fool website, aimed at investors, concerns are spelled out that revenue growth in the UK has slowed despite the increase in marketing spend.

Writer G. A. Chester says: “Purplebricks’ latest numbers look to me to provide a further indication of a trend towards this negative outcome. As such, the results only increase my doubts about the long-term viability of the business model.

“And with management in the process of spending tens of millions on aggressive international expansion, I continue to see it as a stock to avoid.”

Who is Del boy Prete??

Another secret investor in PB.

Has this person seen PB Facebook page?? just go and check the comments and I would urge every agent to check. Thats the real Feedback for the company.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Mike DelPrete is a New Zealander who analyses Prop Tech for a living.

http://www.mikedp.com/

Not that I agree with PB’s business model, because PB pay peanuts to their staff, and because of that, it’ll always be run by monkeys.

Is PB simply the McDonalds of our profession?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Is PB simply the McDonalds of our profession?

No, as when you pay for a burger at McD’s at least you have a decent chance that you’ll actually get a burger!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’m no PB fan but Mike DelPrete is one of the worlds most respected Tech/PropTech analysts. He doesn’t often get it wrong and is an incredibly sharp man.

He produces a lot of very interesting content. Check his website out and sign up to his newsletter.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Please do give an example where he has been right?

Considering the entire Prop Tech industry is smoke and mirrors i would be interested to see where his informed thoughts have come to fruition.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

‘Considering the entire Prop Tech industry is smoke and mirrors’ What a ridiculous statement.

There are plenty of PropTech solutions that make estate agency better for both agents and buyers/sellers. Granted, there are a lot of solutions to problems that don’t exist, purely to make money but there are also many tech features that are great.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Still waiting for an answer …

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Exactly, prop tech doesnt exist. It is a word for describing how estate agents use email and the internet

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Overall, says DelPrete, Purplebricks “is as much an advertising company as it is a real estate company”.

Exactly, a grand for an advert, upfront, no help, no support, no problem solving, no skill, no management of expectations, no chain control, no contacts, no face time, no accountability and no skin in the game.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Slowly but surely Purplebricks are being found out for what they are which is p**s poor at what they do.

Clueless area reps, useless in-office staff and are non existent in sales chasing or checking chains.

just like the rest of the onliners, these lot will blow away like tumbleweeds eventually.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

i completely agree! (if you replace PB with yourself) which would completely explain why you’re not international, constantly expanding and not a household name. happy Christmas tumbleweed!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Ladies & Gentlemen, we have a comedian.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It works…..but for whom? Sure the Brucies have done brilliantly out of it. Sure some vendors feel they have done well, having moved and paid £1500 but at what potential loss in their selling price

All this comes at a cost of hundreds of millions of pounds of investment from outside sources. Alex Springer pumped in £125million and at this stage their investment is worth half what it was.

This model may work in some cases, but on this scale it is not yet proven and not available unless you can use the bottomless pockets of other peoples money. Ask Emoov & Tepilo investors if they feel the model works.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

On course to lose 50 million in a year, not bad at all. A business model we all strive to replicate.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

‘An overall group loss’ of 27.3 million pounds loss is ‘meaningfully profitable’ – What a load of oarlocks!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

“Purplebricks’ core UK market continues to grow and is meaningfully profitable”

He is talking about the UK.

He also says…

“Purplebricks is an international collection of businesses at various stages of growth. In the U.K., Purplebricks’ most mature market, it continues to grow revenues and operating profit. At maturity and scale the business model absolutely works; there is no evidence to support otherwise.”

But them Motley Fool go on to give you evidence that they claim say shows the model doesn’t work. But they are assuming revenue growth will continue at 22% and marketing at whatever it was 30%+?

Just two guys’ opinions and time will tell. On the H1 results they certainly don’t look as though they’re in trouble in the short term as is generally purveyed here.

Admin costs also rose by 30% plus in the UK and neither mentioned that.

What PB call operating margin rose significantly though as they brought in higher margin streams to their revenue. They say there is still more potential to grow this margin,

All comments relate to the UK.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

UK market is faltering = less instructions for 2019. No new investment in PB and those that have, lost massive and can’t sell up and get out without a hit. One investor that sells now, will create a collapse. This is nothing more than spin. If PB have hit the peak of instructions, the only way is down and anyone who thinks they can continue to grow even in a good market is deluded, they will only ever reach a market level.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

>One investor that sells now, will create a collapse

A collapse in what?

Don’t confuse the SP with the viability of the business.

Think of the overseas operations as unprofitable branches and the UK as a profitable branch.

>If PB have hit the peak of instructions,

Not seeing that. Still seeing instruction growth in the UK.

UK Admin & Marketing costs possibly a concern but they can possibly scale back – that remains to be seen. Also increasing the average income per instruction and margins due to more high margin ancillary sales.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

They lost £25 million in 6 months, they had £100 million cash in hand. Unless they do something dramatic to either increase revenue or cut costs they are going to run out of cash relatively quickly. I cant imagine there would be much appetite if they have to raise funds again.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

AgentQ73,

I also see the growing losses from the overseas operations as a potentil issue but Axel Springer invested when the USA & Oz were making losses and I would imagine they had up to date info. I really wouldn’t rule out further investment but if they have to close down overseas operations they still have the UK which is making a profit.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Please define the true meaning profit?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

>Please define the true meaning profit?

Yawn.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Thought so, you haven’t a clue once you are challenged.

“a financial gain, especially the difference between the amount earned and the amount spent in buying, operating, or producing something”.

Now take away investors lumop sums and what does PB offer in the way of profit, then add in profitable viability?

Viability is defines as “the ability to survive”. In a business sense, that ability to survive is ultimately linked to financial performance and position. … it is returning a profit that is sufficient to provide a return to the business owner while also meeting its commitments to business creditors”.

PB case, the answer from known facts todate = NO.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

>Now take away investors lumop sums

Where does your definition say you should do that?

>it is returning a profit that is sufficient to provide a return to the business owner

The point was made in regard to the UK. Both in the article and by myself. Try and focus on what is actually being discussed.

Think of the overseas operations as unprofitable branches and the UK as a profitable branch.

The general consensus by Analysts is that the UK is making a profit. If you are suggesting otherwise then you are at odds with the consensus of Analysts.

I’m sure there is some fundamental issue that escapes you in regard to what a SP actually means. It’s just the price at which buyers are prepared to buy and which sellers are prepared to sell. A measure of supply & demand. It has consequences if a company wants to raise funds but a SP of 1p doesn’t make a profitable company or part of a company as unviable just as a share price of £5 doesn’t make a company viable.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

DelPrete does say that its rate of growth is slowing in the UK: “But at nearly 80,000 instructions per year, it can’t be expected to keep growing at historic rates.

Time for a lesson in business maths on viability:

1 x 8 = 8

1 x 80 = 80

1 x 80,000 = 80,000 or put another way £1,000 fee x 80,000 listing PA = £80m and it cost how much to run in 2018? After you add in all the other income it could raise and corrections it still made a loss of £113K. (credit to Ostrich 17)

Now if you spend all the money you receive ….. that is not profitable, that is surviving as long as the money train doesn’t stop …. enter DelPrete; “it can’t be expected to keep growing at historic rates”. Enter downturn in market, even worse a recession ….. the writing is on the wall it is not a viable business if it can’t make a worthwhile profit now, it won’t in the future. Enter DelPrete; “UK operations are “meaningfully profitable” = utter nonsense.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Woodentop,

>income it could raise and corrections it still made a loss of £113K. (credit to Ostrich 17)

You just repeat what others are saying but you have no real understanding.

Ostrich 17 states “PB have restated previous years sales figures to comply with IFRS15 (introduced January 2018) which knocks £3.7million off 2018 UK Revenue and nearly £2 million off profit for the full year.”

IFRS15 hasn’t been applied to the full year so I can’t understand how Ostrich17 has come up with this loss for FY18. We only have IFRS15 figures for the two 6 month periods to the end of October 2017 and the end of October 2018.

Also, after a quick look I haven’t been able to reconcile the figures from the latest results with his figures. Can you? Using the new standard for the latest 6 month period being reported there is an operating profit of £5.7m compared to £0.8m for the corresponding 6 month period.

I’m sure this £118k figure will turn up here in the future so perhaps we can get Ostrich 17 to explain how he arrives at it.

He does say though

“Because PB reported under the previous accounting standard for 2018, the figures looked better and now they have been revised downwards some of the benefit is carried into this years numbers.”

These actual benefits for the 6 month period being discussed here amounts to an operating increase of 638%.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

CD46

IFRS15 hasn’t been applied to the full year so I can’t understand how Ostrich17 has come up with this loss for FY18. We only have IFRS15 figures for the two 6 month periods to the end of October 2017 and the end of October 2018.

I’m sure this £118k figure will turn up here in the future so perhaps we can get Ostrich 17 to explain how he arrives at it.

Incorrect – PB have revised the figures and published them with their H1 2019 results which is available on their website.

The UK loss is £113k after tax for the year ending 30th April 2018.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Purplebricks and other Online Only Property Listing Companies are proving what they are – VERY Expensive/Loss Making Advertising Portals that despite trying to sell themselves as Estate Agents, have spectacularly proved they are nothing of the sort!

The public know when it comes to their most valuable financial asset they actually need a “Real” High Street Estate Agent rather than a “Virtual Online Only Imposter”.

Purplebricks will NOT be the “last virtual man standing”, they’ll be the “last virtual man falling. Emoov is just the start of the Online collapse.

If Investors have got money to burn then thow it at Purplebricks as they certainly know how to burn through money! …….however any serious Homeseller should only talk to their Local High Street Estate Agent/s – Virtual & Real (Estate Agency) are a world apart, rather like life!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Well its the USA that is likely to be the make or break of Bricks.Some will argue that Axel’s investment is paying for that and even after the payout for the Canadian business ,plenty of cash still to burn.UK self – propelling but is this business worth £440m in isolation?????

I think New York is going to be the litmus test ? Litltle signs yet of gaining much traction but early days

This guy Conrad is an interesting example from Countrywide Bury St Edmunds back to the Bronx.Hands across the pond and would be worth watching for progress

Joined 5 months ago,no deals yet but handling 5 instructions

https://www.linkedin.com/in/conrad-n-pascal-3a61889b/

https://www.zillow.com/profile/conrad-pascal/

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Got to be careful here guys, they are burning lots of money and still have 100 mill in reserve ( that’s effectively another two years trading whilst making this kind of loss) and it’s not working! But hey, they are close on 80k instructions a year so that is taking away bread from our table (not crumbs, loaves) which is sending some of us to be wound up and some to be bought out and others to suffer losses whilst trying to stay in business in the hopes that PB does go pop and we all benefit again.

if you can survive the next three years whilst you wait, it’s a tough market, there is less bread coming to the table so good luck to you all but don’t overly kid yourselves, every 1% market share they gain hurts us all further and irrespective of their losses, they are growing.

Merry Christmas and good luck

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

They are taking business away from agents who haven’t stood up to the plate, easy pickings for PB.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

the most intelligent comment on here Stevie!

the fact is the highstreet is failing, as in the ACTUAL highstreet. There are closed shops all over the place as more and more people prefer the convienience of online companies such as Amazon and having their shopping delivered.

so the footfall that we were all used to; is also disappearing. we all advertise our incredible database of clients…who all use rightmove and have no allegance to any agent in specific. adapt and survive my friend and if you cant offer what PB does there is very little point in sitting there sulking and complaining! 🙂

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You are just so wrong!

The entire online market is 5/6% – Leaving 94/95% to the high street, the public do not have an appetite for it and the cost per lead is too prohibitive which is what CW, Connells and even Quirk have said!

It is an unsustainable business model.

If the online was 95% and High Street was 5% would you say online is failing and High Street is what the public want?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

98% of property searches start online Smile… i’m not talking about market share.

i didnt say that the highstreet estate agent is failing; i said the highstreet is. there are many articles saying that shops’ footfall is down hence why you will see TV adverts now advertising going to your local highstreet.

probably not best to take your stats from CW or Quirk…

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Sorry i have absolutely no clue what your point is!

PB do not offer a single thing the high street do not.

However the high street offer way more than PB.

You are making zero sense.

Please tell me what PB does that is so amazing i cant do from my high street offices. Please just one!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Above I called you a comedian. Sorry, I got it wrong, you’re a clown.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Is this guy for real. Never heard so much tosh to support as business model that 1. Is making a massive loss 2. Always has done. 3. Can never make a profit to recover its O/A losses, they are so massive now. 4. The business solely realise on new business income either from investors (which is what this story really is about, making up a confidence trick) which now have had over 70% wiped off its share price last week, so is no good for trading shares anymore and paid no dividend for those that invested for a stake in returns (there aren’t any) 5. It is a high risk strategy dictated by market conditions. If the market falls, so does its income from instructions … hello. There is only so much property it can ever hope to list. 6. If as suspected they are not as good at selling to completion and the public find out ….. bye, bye. This guy must be the Ostrich with his head in the sand.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

All the signs suggest that 2019 will be far tougher than 2018, with the government intent on pulling in the reigns of the housing market. Maybe revisit this this post in 12 months; it wouldn’t surprise me if PB, in it’s current form, had gone to the wall….. After all what fool pays upfront in such a tough market?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Not sure about the sales graph used by Mr. DelPrete – he is comparing apples with pears.

PB have restated previous years sales figures to comply with IFRS15 (introduced January 2018) which knocks £3.7million off 2018 UK Revenue and nearly £2 million off profit for the full year.

Because PB reported under the previous accounting standard for 2018, the figures looked better and now they have been revised downwards some of the benefit is carried into this years numbers.

For 2018, the revision means PB UK made a loss of £113k after tax and the group loss was £30 million.

They probably have about £75-£80 million cash left after paying £11 million for the Homeday.de JV.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Spin that one Ducky?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I don’t spin things. See my earlier comments.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Lol.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I did and they are spin. Using the argument because someone’s said it, anyone else who then says it is wrong. That’s what you do all the time with quoting PB.

I’m waiting for HMRC to ask where has roughly £40 million revenue gone from the 80,0000 instructions THEY said THEY had in 2018 as THEY have declared only 50% revenue?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Bury your heads in the sands quotes above!

PB should not be underestimated and deserve respect for doing what no other estate agency business has ever done, secure 80,000 instructions a year after only four years of existence.

They do present an opportunity for those of us who can see it, otherwise, the “bury your heads” brigade will continue to bleat, not change and wonder why their turnover is going down.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Good point and possibly 50% ended up back in the High Street market?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Exactly what change are you proposing for the industry?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

To be fair the amount they spend on advertising 80,000 is small fry.

They spend more on advertising than any other estate agency.

If they were in line with other firms they would not be around for more than a couple of months Emoov and Tepilo have proved that. They burn cash at an incredible rate.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Exactly, their model is about volumes, something the investors in Emoov & Tepilo were never able to achieve.

PB UK now paying their massive admin & marketings costs with revenue and now decreasing the cost of sales as a percentage of turnover by adding high margin revenue streams.

“During the First Half, we created a Home Purchase team, replacing and enlarging the existing Conveyancing Sales team, with an enhanced customer proposition, utilising sophisticated data resources to engage with buyers, sellers and viewers. This team is focused on driving ancillary sales predominantly to buyers. As can be seen from our First Half results, the investment is showing a good early payback, with UK ancillary revenues in the period increasing by 25% year-on-year. This growth has been primarily driven by early success in selling conveyancing services to the buyer. Some progress has been made with mortgage referrals, though this opportunity remains in its infancy. There still remains a significant opportunity with conveyancing and mortgages to further drive revenue and margin.”

Lettings revenue also up in line with general growth of revenue.

“Lettings represented 8% of UK revenue in the First Half (H1 2017: 8%) and we continue to develop our capabilities with 5,800 units under management at 31 October 2018, up 32% year-on-year (31 October 2017: 4,400). We have recently strengthened our management of this team to examine ways to further scale the business and our national network of Local Lettings Experts. Our intention is to provide an opportunity for Landlords similar to what we offer Sales Vendors with service excellence and delivery.

The legislative risk to tenant fees is not expected to have a material impact on the business.”

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

BUT THEY HAVE LOST 27 MILLION IN 6 MONTHS!!!!!!

Even if they stop the loss over the next 6 months how long will it take them just to claw back the last 6 months loss?.

It is a business that does not work.

Give any agent 50 odd million in a year and they will make a profit somewhere in their business even if just solicitor referals, the accountants can also make one part of the business is doing well when maybe its not.

I have a small group of offices and a letting division. if i have central overheads i can chose where to offset them.

PB is not a viable business, it is an investment vehicle for the board / investors. They have milked it wonderfully but they will never be a sustainable business.

IT JUST WONT WORK

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

>BUT THEY HAVE LOST 27 MILLION IN 6 MONTHS!!!!!!

>Even if they stop the loss over the next 6 months how long will it take them just to claw back the last 6 months loss?

All very approximate and loosely put…

if you look at the UK PB have lost £5.4m in 2015, £10.5m in 2016, made £1,7m in 2017 and made £8.1m in 2018 and £5.7m in H1 2019.

So it won’t take that long if the other markets follow suit at the same pace. If it doesn’t work out overseas that won’t be a surprise, lots of businesses fail to reproduce what they’ve achieved at home when they try overseas. It looks to me that both the £50m investment and the £125m investment were allocated nearly totally for investment in the overseas businesses. So the UK’s been standing on its own feet for a while now.

I haven’t looked at the results properly yet but a quick look says the USA had revenue of £5.9m and made a loss of £20m. Look at the UK in 2015 and they lost £5.4m on revenues of £3.4m. So all things being equal you’d say it will take longer in the USA if it’s going to happen.

But you do get the feeling they are throwing money at the USA. They accelerated growth with the £125m raised by Axel Springer. And if you look at the UK they have a dominant position now with it unlikely they will have any serious competition. So perhaps the accelerated rate of investment is to do with taking #1 position and making it less attractive for competitors.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

These are not THE REAL AND TRUE figures, are they Ducky or are you doing a bit of spin after all.

if you look at the UK PB have lost £5.4m in 2015, £10.5m in 2016, made £1,7m in 2017 and made £8.1m in 2018 and £5.7m in H1 2019.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

>These are not THE REAL AND TRUE figures, are they Ducky or are you doing a bit of spin after all.

I said they were very approximate and lossely presented. Taken from the financial reports for 2016 & 2018. If there are mistakes then correct them.

I’m not going back to check now but it is not the actual numbers that are important, just the fact they have moved from loss into profit in the UK. This shows the UK is a viable business and gives a timeframe for the process of loss to profit that the overseas businesses need to try and emmulate.

If the figures that are available don’t demonstrate this point then feel free to show the correct figures and I’ll discuss.

Like I say, I don’t spin. Only interested in the truth. I do my own research, keeping track of instructions in both the UK, Oz and the USA to varying degrees of accuracy and frequency with the UK being the most closely followed. Like I say, if I’ve made a mistake or you know something I don’t then just put it into the discussion.

I will presume the figures are as per the results if I don’t hear from you.

.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

UK corrected loss £113K for 2018. AND near 80,000 instructions plus other income source does not equate to £48,300,000 revenue in UK. Where has the other 50% suddenly disappeared!!!!!! You can spin EBITDA in accounts, it means nothing in the real world, you either made a profit to cover your liabilities or you didn’t.

EBITDA “an accounting measure calculated using a company’s net earnings, before interest expenses, taxes, depreciation, and amortization are subtracted”.

As usual every time you put finger to keyboard you shoot yourself in the foot, as does all the propaganda that comes out of PB who, like you keep telling us that 1 + 1 = 3.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Woodentop,

You clearly misunderstand how the new financial reporting works. All it does is move the timing of certain elements of the turnover. This change in reporting standard applies to every business.

You can’t mix the standards so to be consistent over the years, for comparison purposes you have to use the old standards. Comparing like for like. That’s what I did.

If you like the new standards better then that means for the latest results revenue grew by 39% rather than the 22% if the old standards had been used. Operating profit grew by 638% rather than the 78% using the old standard. You takes your pick but don’t pick and choose which one suits your argument, that really is spinning the truth.

It seems like you read what others are saying but don’t really understand, just throwing around what you’ve heard from others. In regard to moving from loss into profit the figures, both using the old standards and the new speak for themselves. Is there anybody who knows what they are talking about who is claiming that the UK is not in profit?

I used operating profit for my comparisons. Feel free to use another or discuss the issues that you have with using operating profit for PB’s results (not just a general comment you’ve found somewhere online).

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

PB have revised the figures and published the UK loss at £113k after tax for the year ending 2018 and available on their website.

Again 80,000 UK instructions equates to £80m revenue, yet only half is declared. No doubt it will appear in 2019 accounts to try and make that year look better than it is, when it should have been reconcilled.

The only people who is spinning is PB and you in an attempt to justify your constant mistakes every time you post.

I see the share price has not recovered after a week, a slight rise of a few pence but sharp dive on close Friday still equates to roughly 70% loss of share value in 2018.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Purple Bricks spent all that money on a rebrand and forgot to put a telephone number on their boards.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I think it was deliberate.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I thought they were proper estate agents. All the estate agents I know have a number on their boards 😉

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Aye, and you can call them. Just imagine this…… How long do you spend on the telephone trying to sell a property? How long do you spend on the telephone taking calls from enquiries about a property from prospective buyers? How long do you spend on the telephone keeping your vendor happy? Now forget about all the other calls you do in a day like take-ons, photography, EPC’s, sales brochures, web uploads, chain checks, chasing sales, offers, break for lunch, going to the toilet, viewings, having a natter about what you did last night etc, etc, etc.

Anyone who says they, “an on-line only agent” who can do the same job as the High Street with 80,000 listings and answer the phone …. give me a break. They are purely an advertrising model, not a service businsess within a service industry. Pay cheap, you get cheap service or as they really are … nothing more than a listing company for private sales by owners and have tapped into the power of TV advertising (that is their success) and fooled the public they are the same as the High Street and use every bit of revenue to try and keep afloat. However one wishes to spin it … they are always on the brink of collapse without outside investment and a poor housing market/recession will see them off just as quick as Emoov.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Interesting point about the phone number. More and more agents in our area are not putting their numbers on the board as they want site visitors…….

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Fatal mistake, you actually want to TALK to people. Then you have a great chance of converting the LEAD in to money.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

What do you know about money PropertyPundit?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Apply a full 20% VAT return based on PB’s above turnover of £48,300,000 =£9,6660,000 plus all other actual costs and are they still making a profit?

I gather that HMRC shall soon be asking a lot more questions from people claiming to be self-employed which may have devastating consequences for any business that uses such facilitators for a large unified brand providing all their income many of whom are not likely to be VAT registered?

Is using £10s of millions of other peoples money over many years to buy market share anti-competitive as the vast majority of traditional agents do not have access to such funds to prop them up particularly as traditional agents only charge on completion of their contracts?

Surely the real disruption to the market is that 10,000s of users now pay whether they move or not and may end up paying two estate agency fees or losing their fees altogether if the company goes bust?

Around 80% of sellers are buyers so presumably many of their conveyancing referral ‘commissions’ double up for sale and purchase ie £800 plus?

Are any of these vast fees paid in full or in part to separate companies thereby possibly depriving their shareholders of a valuable income stream that would not be possible without their estate agency network?

PB owners have proved that this model works for them but does it work for the majority of their customers?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Sorry, too many 0s posting above ought to show £9,666,000.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

There is one thing that PB cant spin. And that is the number of people putting their houses onto the market which next year is going to be less than this year.The more “traditional” pay on results agencies who do not sell a property then is it that the vendors of that property are more than likely to move to another No sale No Fee agent. I have not had anyone move from my books to a pay upfront agent but lots form PB to me. So PB do not get any of the market that fails-which is what 50% ? churn-so wholly reliant on new entrants to the market.

PLUS-as illustrated beautifully by Emoov in terms of company value-there is none- as all revenue is as we(and PB customers know!) is taken upfront- PB cant really sell all/parts of the business as its only as good as last months new instructions(lettings is a disaster by all accounts).Its a doomed business model-I sold out at 3.53 thank god!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I have a geunine question regarding PB being profitable in the UK.

How difficult would it be to apportion some of the costs/overheads of the UK operation to the US/Australia losses? Both US and Australia are expected to show losses right now as they are growth businesses. PB would appear to have an invested interest in showing the UK to be profitable in order to provide hope to investors that in the long term the whole group can be.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

No doubt some of the HO costs are charged out to subsidiary companies – e.g senior management and other group admin/marketing costs.

You have to rely on Grant Thornton undertaking a rigorous audit of transfer pricing policy and related transactions.

Under IFRS15 – restated revenue for 2018 means PB UK made a loss of £113k after tax last year.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Ostrich17 so an adjusted loss now in UK in 2018.

Do you think the markets are aware of this profit to loss adjustment for a further year which now means they have never reported a year-end profit in the UK?

Material information which may have mislead the markets?

Why didn’t Grant Thornton allow for IFRS15 at the time of reporting?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

These are unaudited Half Year figures produced by PB – Grant Thornton will audit at the year end and restate the numbers in next years accounts for comparison purposes.

IFRS15 is effective from January 2018 – it is not misleading the markets, simply a change in the timing of declaring sales revenue from contracts with customers. E.g. Conveyancing revenue will be received much later than instruction revenue.

Frustratingly, PB have not included their favourite KPI’s in the results for the half year and other effects are difficult to deduce from the available info.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Thanks, O17, understand now.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

As previously posted; there are some scurrilous and totally unsubstantiated rumours that PURP are doing precisely that (or not, as the case may be).

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Put yourself in the position of a consumer or investor and consider, based on these facts/ research, ask yourself; “would I pay upfront/ take out a loan to use this company to sell my home/ would I invest in a business model which is the transactional customer proposition equivalent of a £1,100 “coin toss”.”

“the Av house price in the UK is £232,554” Source @HMLandRegistry Sept 2018

“The national Av (estate agent fee) is now 1.06%. (Inc VAT)” Source @netanagent via Property Industry Eye

Av cost per completion per customer High St. agent = £2,465

Av cost per completion per customer with @PurplebricksUK #purp = £2,231

Based on Jefferies (conservative) 51% listing to sold (legal completion) ratio of 51% and PURP published revenue per customer figure of £1,138

Therefore “saving” per sale (if you are one of the lucky 51%) = £234 on a £1,138 upfront gamble with Purplebricks

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Are the public wise to the fact that the difference in cost between PB and the High Street is marginal ? (see other lead story today on EYE). When there is next to nothing in price, research has proven that consumers judge quality as the deciding factor. If agents are not getting the message over to the consumer, quality of service they offer … who’s fault is that! PB gained traction by selling the idea they can do the job for less … hasn’t that argument now gone out the window?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Isn’t that a misleading comparison Chris?

Do you include income from ancillary products for traditional agents?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It’s not working for those that bought shares in January of this year.

This companies shares aren’t even fully liquid, Woodford has 30% of the company locked up. When he bails out and given his other woes he will have to at some point the shares can only continue their downward spiral.

This ‘prop tech’ commentator, some bloke sat at home in his dressing gown and slippers who alternates between his laptop and watching Cash In The Attic on Dave should do some proper research.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It is reported that should Woodford try and sell les than 1% it will trigger a Red Flag at the market. I read that to mean bail, bail, bail …… shares will go into freefall?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

By their own figures they are loosing over £1 million every week. Bail, bail bail in anyone’s language!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

The shares are up again today. There must be some positive news filtering through about the PB performance stats for the boys in the city to be finding that silver lining that we cannot see.

A slow start next year will hit the SP hard again, and many pundits see it dipping if you look at share chat sites.

Real Estate Agents need to focus on the client and not the cash and they will be fine.

Fake agents, well they can do what they do. They don’t bother me in the slightest.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Up 1.20p today, that’s 0.8%.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I finally saw my first Emoov for sale board today……Doh!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register